What a year it’s been for the banking industry! From threats from outside the industry by Apple and Wal-Mart, to questions on whether Colorado and Washington banks should work with legal marijuana businesses, to regulatory shenanigans at the New York Fed, 2014 has been memorable. As the holidays approach and I think back on the year that was, I thought I’d take a few minutes to share some of the banking-related stories I enjoyed in 2014.

Regulations

- Banks given the go-ahead on working with marijuana businesses: Marijuana may be legal in some states, but that doesn’t mean banks are ready to work with marijuana businesses.

- How to Punish a Bank: This is from National Public Radio’s Planet Money, so it’s more of a listen than a read, but delves into the problems of effectively punishing the big banks.

- Bank of America Adds a Mortgage Settlement to Its Collection: Bloomberg’s Matt Levine (also cited in the NPR segment) provides the data on (at the time) Bank of America’s $68 billion in mortgage settlements, and asks how effective these penalties and fines are when they become business-as-usual.

- Inside the Emerald City: Jack Milligan, editor of Bank Director, delved into the culture of the NY Fed following concerns that regulators got just a bit too cozy with the big banks they oversee.

NonBank Competition

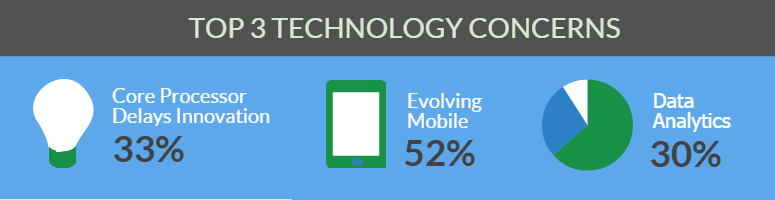

- Sizing Up the NonBank Threat: Jack Milligan’s cover story in the 4th quarter 2014 issue of Bank Director magazine was a great way to close out a year that saw a lot of focus on the impact that nonbank competitors, from Wal-Mart to Apple, had on traditional banks.

- Are Wal-Mart and Apple poised to be regulated by the CFPB?: This Washington Post article feels particularly prescient, following news of the Consumer Financial Protection Bureau’s lawsuit against Sprint.

- For Banks, the Sky is Falling: Al Dominick’s blog, AboutThatRatio.com, explored the nonbank threat in a five-part series that examined Facebook, PayPal, Wal-Mart and crowdfunding.

- Wal-Mart’s Getting into Banking, and It Makes a Lot of Sense: FiveThirtyEight delves into data on the unbanked to explain Wal-Mart’s expansion of its financial products.